Finance Function in the Era of Agentic AI

Imagine your finance team is in the middle of the month-end close. The numbers are already in the ERP, but some entities haven't submitted their data, accounts with unexplained variances remain, and emails are piling up as you chase status updates from various controllers. This is a familiar scene in many companies. The process is repetitive, deadlines are tight, controls are formal, and the impact is directly felt on operational quality. Until now, the solution has been partial automation: workflow engines, RPA, dashboards, and the occasional copilot for drafting. These help, but they haven't fundamentally changed how finance works.

Now, the question is starting to shift. It's no longer "how do we speed up finance tasks?" but rather "how do we redesign finance operations so that digital labor can participate in closing, reconciliation, invoice handling, and reporting without breaking controls?" This matters because finance is not a domain suited for wild experimentation. An agent in finance cannot be a "smart assistant" that produces convincing but unauditable answers. If used in this function, agents must operate as part of a disciplined operating model: connected to the ERP and supporting systems, subject to policies and thresholds, producing evidence packs, and keeping humans in the loop at the right points of judgment.

Why Finance Is a Strong Candidate

Finance is one of the most suitable enterprise domains for an agentic approach, precisely because it is structured but not entirely simple. On one hand, finance involves a lot of repetitive work: matching transactions, checking document completeness, tracing the causes of mismatches, drafting variance explanations, reminding process owners, and routing exceptions to the right parties. On the other hand, finance is full of controls: approval matrices, segregation of duties, materiality thresholds, audit trails, and documentation requirements that are far higher than in many other functions.

This combination makes finance attractive. Many of its activities are clear enough for an agent to assist with, but they don't necessarily need to be fully automated right away. This is what is called bounded autonomy: agents can read, compare, prepare recommendations, and orchestrate follow-ups, while humans retain judgment, approval, and ultimate accountability.

If we look more closely, much of the work in finance isn't really about "calculating numbers." It's about managing exceptions and context. During the close, the numbers are already in the system, but the team still needs to check for missing inputs, find late entities, understand which accounts are deviating, request explanations from business controllers, and then build a narrative strong enough for review. During reconciliation, the system can show mismatches, but someone still needs to trace the cause, compare transaction sources, check for timing differences, and prepare proposed journal entries or follow-up actions. During invoice processing, OCR and legacy workflows may handle part of it, but exceptions remain high when there are PO mismatches, goods receipt issues, tax problems, vendor anomalies, or policy deviations.

All of these are areas where agentic AI is more useful than static automation. Agents can pull data from multiple systems, read policies and case histories, reason about the cause of an exception, prepare draft actions, and escalate only when necessary.

Why Finance Doesn't Have to Wait for "Full Autonomy"

Many finance leaders hesitate because they think agentic AI means handing decisions over to machines. That's the wrong framing. For finance, the biggest initial value comes from a more conservative model: the agent as a close monitor, an investigator of mismatches, a preparer of evidence and drafts—not directly as the final decision-maker. This approach is a better fit for the reality of the finance function. Human control isn't lost, but the burden of repetitive manual work is reduced. Finance teams can shift from administrative tasks and repetitive follow-ups to analysis, control judgment, root-cause resolution, and business partnering.

Despite the promise, not every area of finance is a good starting point. The agentic pattern is less suitable if the underlying process itself isn't stable, the chart of accounts and data definitions are chaotic, accounting policies aren't well-documented, or the organization lacks consistent discipline in approvals and audit trails. In such conditions, an agent will only accelerate the existing confusion. Finance needs a sufficiently mature process and data foundation before giving agents an operational role.

Three Primary Use Cases: Close, Reconciliation, and Invoice

For many companies, the three most sensible starting points are the close agent, the reconciliation agent, and the invoice agent. All three have real workloads, clear business value, and a healthy scope for bounded autonomy.

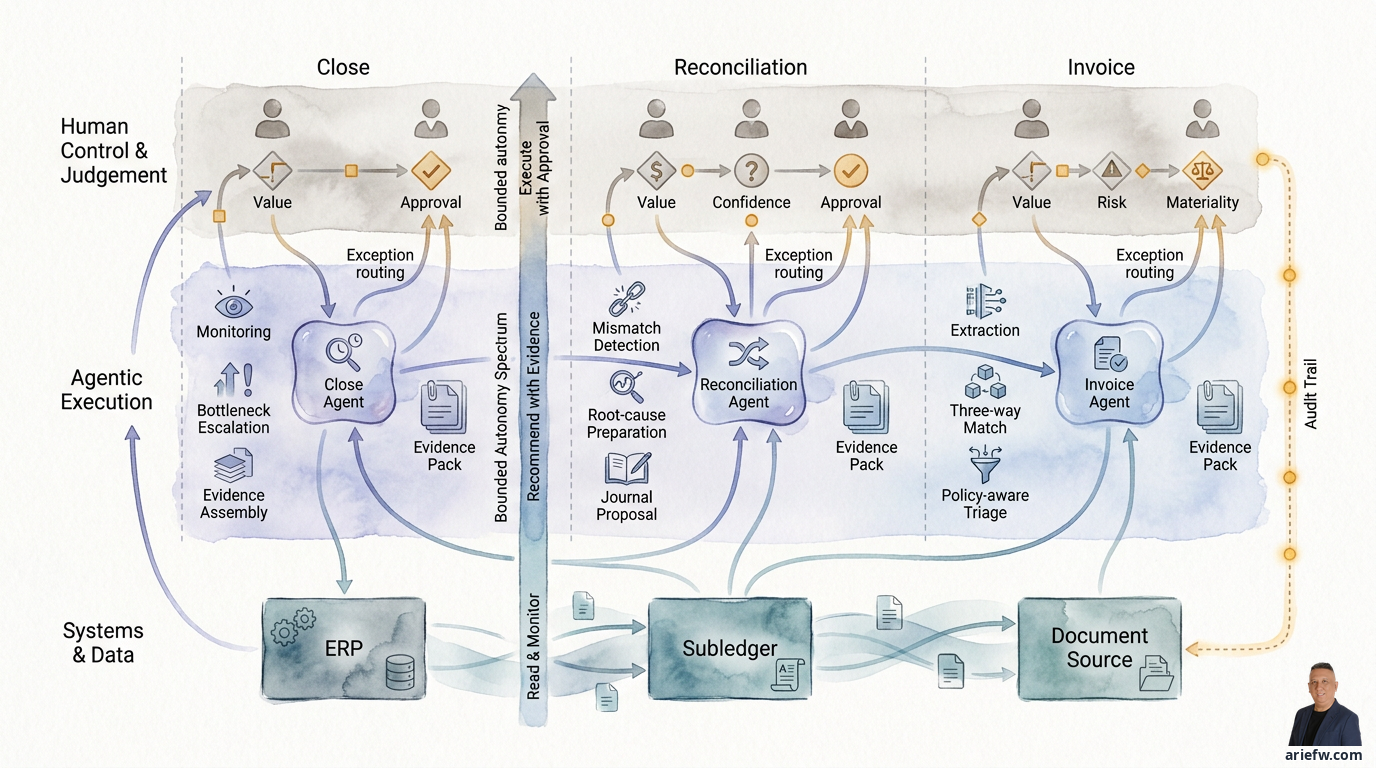

1. Close Agent: From Close Calendar to Close Orchestration

In many organizations, the month-end close still relies heavily on manual coordination: spreadsheet trackers, email follow-ups, status meetings, and chasing inputs from various entities or functions. A close agent can act as an operational orchestrator for this process.

Practically, a close agent can monitor close tasks and due dates, check for missing inputs from the ERP, subledger, or consolidation tool, flag accounts or entities with unusual variances, remind late process owners, gather supporting evidence, and prepare draft commentary for reviewers. For example, a multi-entity group has a close process involving AP, AR, inventory, payroll, and accruals. The close agent checks whether all feeds have been received, detects that one entity hasn't completed its intercompany elimination, and escalates the bottleneck to the regional controller. At the same time, the agent prepares a list of accounts with the largest variances and pulls the previous month's commentary history as initial context.

The primary value of a close agent isn't just "making the close automatic." It's about reducing time lost to chasing, decreasing blind spots on bottlenecks, improving the quality of variance explanations, and making reviews more focused on judgment rather than data gathering. However, a close agent is suitable for monitoring, evidence assembly, and drafting. It is not suitable for autonomously determining material accounting treatments. If there are issues like revenue recognition, impairment, reserve judgments, or significant accounting interpretations, humans must remain the decision-makers.

2. Reconciliation Agent: From Mismatch Detection to Root-Cause Preparation

Reconciliation is a classic area often full of manual work. Systems can show that two sources don't match, but finding the cause of the mismatch still takes time. This is where a reconciliation agent provides value.

This agent can compare transactions across sources, categorize mismatches by pattern, distinguish timing differences from actual errors, search for possible causes like missing postings, duplicate entries, currency issues, or mapping problems, and then prepare proposed journal entries or corrective actions for human review. In bank reconciliation, the agent compares cash movements in the ERP with bank statements, finds several uncleared items, and groups them into those likely to be outstanding timing differences and those that appear to be posting errors. For certain items, the agent prepares a journal proposal complete with source transaction references. Another example is intercompany reconciliation: the agent compares AR/AP between entities, flags mismatches due to cut-off differences, and prepares a list of exceptions that truly need to be discussed by the controllership team.

Reconciliation isn't just about matching. It's also about reading patterns, tracing history, connecting multiple sources, and preparing hypotheses about causes. Static automation often stops at "match / no match." An agentic pattern can go further into exception investigation. The greater the agent's autonomy in preparing journal proposals, the more important it becomes to have controls over the source data used, confidence levels, materiality, and approval paths. For low-value mismatches with very clear patterns, the agent might be safe enough to prepare a draft correction. For material items or ambiguous patterns, the agent should stop at a recommendation and evidence.

3. Invoice Agent: From Capture to Policy-Aware Processing

Many organizations already use OCR or invoice workflows. But exceptions remain a major source of workload, especially in AP. An invoice agent can go beyond simple document extraction.

This agent can read an invoice, extract key fields, match the invoice against POs and goods receipts, validate vendor, tax, and payment policies, check for deviations from contracts or thresholds, and then prepare the appropriate approval or escalation. For example, an invoice from a vendor arrives without a clear PO reference. The agent checks the vendor history, active contracts, and spending category, and concludes that the invoice is likely related to a recurring service that should use a specific contract. The agent flags the policy deviation, prepares a case summary, and routes it to the correct approver. In another case, the invoice matches the PO and goods receipt, the amount is low, the vendor risk is low, and there are no anomalies. In a more mature design, the agent can prepare a straight-through processing path with predefined controls.

If the vendor master is poor, PO discipline is low, or many purchases are made outside the official process, the invoice agent will constantly face structural exceptions. In such situations, the agent is still useful for triage, but don't expect high touchless processing rates before the procurement and AP process discipline is improved.

Control and Audit: A Prerequisite, Not an Add-On

In finance, the quality of an agent isn't measured solely by how often it is "correct." What matters more is whether every recommendation or action can be accounted for. Therefore, finance agents must be built with control and auditability as core design principles.

Evidence Pack for Every Recommendation

Every time an agent makes a recommendation or prepares an action, it should generate an evidence pack sufficient for human or internal auditor review. The contents of an evidence pack typically include the source data used, reference documents or transactions, the policies or rules checked, a summary of the reasoning behind the recommendation, a confidence level or degree of certainty, and the required approval status. In reconciliation, if the agent proposes a journal entry, the reviewer must be able to see the source transactions, the mismatch logic, the affected accounts, and the reason the proposal was made. In invoicing, if the agent flags an invoice as ready for processing, the approver must be able to see the three-way match results, vendor status, policy checks, and the rationale for why the case is considered low-risk or an exception. Without an evidence pack, the agent is just a suggestion generator. That's not sufficient for finance.

Approval Thresholds Must Be Risk-Based

Approval for finance agents should not be determined simply by "allowed or not allowed." A more appropriate approach is a tiered threshold based on several factors: transaction value, agent confidence, vendor risk, materiality, account or process type, and whether the case pattern is familiar or new. A healthy design example: low-value invoices from trusted vendors with a complete three-way match and high confidence can go through a light approval path; high-value invoices or new vendors must still go through full human review; journal proposals for non-material accounts can be reviewed by an analyst; proposals touching material accounts or judgment areas must be escalated to a controller. This approach is more realistic than forcing all cases to be treated the same.

Audit Trail Must Connect the Entire Decision Chain

The audit trail for a finance agent should not just store the final output. It must connect the source data, the tool/API calls made, the policy checks performed, a summary of the reasoning, any human approval or override, and the final result entered into the system. This is important for three reasons. First, internal control: the finance team must be able to trace why an action occurred. Second, auditability: internal audit or external auditors need to see that the agent operated within testable boundaries. Third, continuous improvement: if the agent makes a mistake, the organization must be able to understand whether the problem lies in the data, policy, integration, or workflow design.

A common mistake is starting with the ambition of "touchless finance" without first establishing delegated authority, segregation of duties, a policy engine, and adequate observability. For finance, a healthier sequence is to start with read, monitor, and draft; then move to recommend with evidence; and only in specific areas progress to execute with approval or execute with monitoring. If the sequence is reversed, trust will collapse quickly.

Realistic Outcomes: Not Finance Without Humans

The least helpful narrative for the finance function is that agentic AI will "replace the finance team." A more realistic and useful perspective is to look at the change in outcomes and the change in roles.

Reasonable targets for a finance agent pilot typically include a faster close cycle time, a reduced exception backlog, less manual follow-up, better quality variance explanations, and reviews that are more focused on material items. These are outcomes that can be directly felt by controllership, shared services, and business finance teams. During the close, controllers no longer spend most of their time chasing status and gathering evidence, but instead focus on accounts that truly require judgment. In AP, analysts are no longer buried in simple invoice exceptions, but handle cases that genuinely need policy interpretation or coordination with procurement and vendors. In reconciliation, teams no longer start from a raw list of mismatches, but from exceptions that have already been categorized and given a hypothesized cause.

If agents are used correctly, the human role in finance shifts to three main areas. First, analysis: more time to understand business drivers, not just prepare data. Second, control judgment: more focus on decisions that require professional judgment. Third, business partnering: more capacity to engage with business units on the implications of numbers, risks, and corrective actions. This aligns with the finance transformation direction that many CFOs have long desired: reducing the transactional burden and increasing analytical contribution. Agentic AI provides a new way to achieve this, but only if controls remain strong.

A 90-Day Roadmap for a Finance Agent Pilot

The best approach for finance is not to start with a large platform, but with a narrow, operational pilot.

On days 1–30, select one use case with a healthy combination of value and risk, such as close task monitoring, AP invoice exception triage, or reconciliation preparation. Map out the source systems, required data and documents, relevant policies, approval thresholds, and the points where humans must retain decision-making authority. The output of this phase should not be a demo, but a workflow design and control model.

On days 31–60, build the agent in draft or recommend mode. Connect the agent to the necessary data and tools, but limit its autonomy. Focus on evidence packs, audit trails, exception dashboards, and regular reviews with the daily or weekly finance users. In this phase, success is not measured by full automation, but by whether the agent's output is truly usable by the finance team.

On days 61–90, run a limited pilot on a subset of entities, vendors, accounts, or specific case types. Measure time saved, recommendation acceptance rate, correction rate, exception backlog, and evidence quality. At the end of 90 days, the decision to make is not "is the AI good?" but whether the use case is worth expanding, whether the level of autonomy can be increased, or whether the data/process foundation needs to be improved first.

Practical Checklist

Decisions to Make Now

- Choose the right initial finance use case. Start with close monitoring, reconciliation preparation, or invoice exception handling—not material accounting decisions.

- Define the agent's autonomy boundaries. Explicitly decide whether the agent will only read, prepare drafts, make recommendations, or execute specific actions with approval.

- Design the evidence pack and audit trail from the start. Don't wait for an audit or internal control inquiry to think about documentation.

- Establish risk-based approval thresholds. Use a combination of transaction value, confidence, vendor risk, and materiality, not a single uniform rule.

- Prepare for the change in finance team roles. Ensure the pilot isn't just about chasing efficiency, but also about shifting team capacity towards analysis, control judgment, and business partnering.

Quick Readiness Checklist

- The chosen finance process is sufficiently stable and documented.

- Source data from the ERP, subledger, or supporting systems is reliable enough.

- Relevant policies and SOPs are available and can serve as a source of truth.

- The approval matrix and delegated authority are clear.

- The finance team is willing to review agent output and provide structured feedback.

- There is a business owner and a technical owner for the pilot use case.

- Audit trails, logging, and evidence packs are designed before production.

- The pilot scope is limited to specific entities, accounts, vendors, or case types.

- Success metrics include cycle time, backlog, acceptance rate, correction rate, and explanation quality.

- Internal control, risk, or internal audit teams are involved from the start.

Red Flags Before Scaling

- The organization wants to give the agent broad execution authority in finance immediately.

- Master data, policies, or the chart of accounts are still inconsistent.

- There is no clarity on who approves the agent's recommendations.

- The agent produces suggestions, but there is insufficient evidence for review.

- The pilot is evaluated only on the amount of automation, not on the quality of controls and outcomes.

- The finance team sees the agent solely as a threat to their roles, not as a tool for redesigning work.

Reflective Questions for CIOs, COOs, CFOs, and Transformation Leaders

If your company's finance function still spends too much time on chasing, matching, follow-ups, and preparing explanations from scratch, is the real problem a lack of tools—or is it that the finance operating model hasn't been designed to leverage digital labor in a controlled way? That's the question that needs to be answered before agentic AI is taken further into the finance function.